The EU Carbon Levy (CBAM) took effect January 2026. Learn how Indian exporters of steel, aluminum, and cement can navigate compliance, costs, and the 5 key assurances India secured from the EU

The European Union’s Carbon Border Adjustment Mechanism (CBAM), widely referred to as the EU carbon levy or carbon border tax EU, entered its definitive phase on 1 January 2026. For Indian exporters of iron and steel, aluminium, cement, fertilisers, hydrogen, and electricity, this marks a seismic shift from mere reporting to real financial and compliance obligations. Although the levy is formally paid by EU importers through the purchase and surrender of CBAM certificates, the economic burden frequently passes downstream to non-EU suppliers in the form of lower realised prices, stricter contract terms, and selective sourcing.

This essential guide outlines everything Indian exporters need to know about EU CBAM for Indian exporters in 2026 and beyond. With India’s steel and aluminium exports to the EU already declining 24% in FY2025 due to anticipation of the levy, proactive preparation is no longer optional—it is a survival imperative for maintaining market access in one of India’s most premium destinations.

Understanding the EU Carbon Levy (CBAM)

What is CBAM?

The Carbon Border Adjustment Mechanism is an important policy by the European Union to stop “carbon leakage.” This happens when EU companies shift production to countries with less strict climate rules, or when EU products get replaced by imports that cause more carbon emissions.

Simply put, CBAM ensures that imported goods face the same carbon costs as products manufactured within the EU. It achieves this by requiring importers to purchase CBAM certificates corresponding to the embedded emissions in their goods, effectively applying a carbon border tax EU on carbon-intensive imports.

Why Does CBAM Matter for India?

India’s relevance to this discussion stems from the carbon intensity of its industrial sector. Indian steel and aluminum production relies heavily on coal-based processes, making them more emissions-intensive than their European counterparts. This means the EU carbon levy will impose a proportionally higher cost on Indian goods compared to those from nations with cleaner production methods.

The Core Challenge: Indian blast furnaces emit more carbon than European ones. This could cost the Indian steel industry an estimated ₹50,000 crores in additional carbon taxes.

High Exposure Sectors: Why Indian Exporters Are Particularly Vulnerable

India’s export profile aligns closely with CBAM’s scope, making the carbon border tax EU a direct threat to competitiveness. CBAM Reporting Impacts on Businesses are already being felt across the following sectors:

- Iron & Steel: Accounts for the bulk of exposure, with annual exports to the EU valued at around €4.2 billion pre-CBAM pressure. High reliance on coal-based production results in elevated emission intensities.

- Aluminium: Significant volumes (around €800 million annually), where electricity-intensive smelting drives indirect emissions.

- Cement and Fertilisers: Growing but notable exposure, especially for downstream products.

Estimates suggest CBAM could add 3–8% (or more) to product costs depending on emission intensity, with some analyses indicating Indian exporters may need to absorb 15–22% price reductions to keep EU buyers whole after certificate costs. For a mid-sized steel exporter shipping 50,000 tonnes yearly, this could translate to hundreds of thousands of euros in effective annual impact by 2030 if no decarbonisation occurs.

The levy does not apply directly to Indian firms, but EU importers increasingly demand verified, plant-level emission data. Non-cooperative or high-emission suppliers risk being de-listed, especially as defaults are phased out post-2027.

The MSME Blind Spot

One major worry for Indian exporters about the EU CBAM is how it affects micro, small, and medium enterprises (MSMEs). These smaller exporters often do not have the money for costly emissions checks. If they cannot provide verified data, the EU uses “default values,” assuming the product comes from the worst-performing factories in that sector.

Critical Warning: Default values assume emissions equivalent to the worst-performing 10% of EU installations. For Indian secondary steel producers, this could make their goods 30-40% more expensive overnight.

How the EU Carbon Levy Calculates Costs

The Mechanics of CBAM Pricing

Understanding how the EU carbon levy calculates costs is essential for financial planning. To simplify this complex process, many exporters are now utilizing a CBAM Tax Calculator to model various scenarios. The basic formula remains:

CBAM Liability = (Embedded Emissions × EU ETS Carbon Price) – (Carbon Price Already Paid in India)

Currently, the EU Emissions Trading System (ETS) carbon price hovers around €83-92 per tonne of CO₂. For Indian exporters without a domestic carbon price (more on India’s developing system later), the calculation is straightforward: pay the full EU ETS price on all embedded emissions.

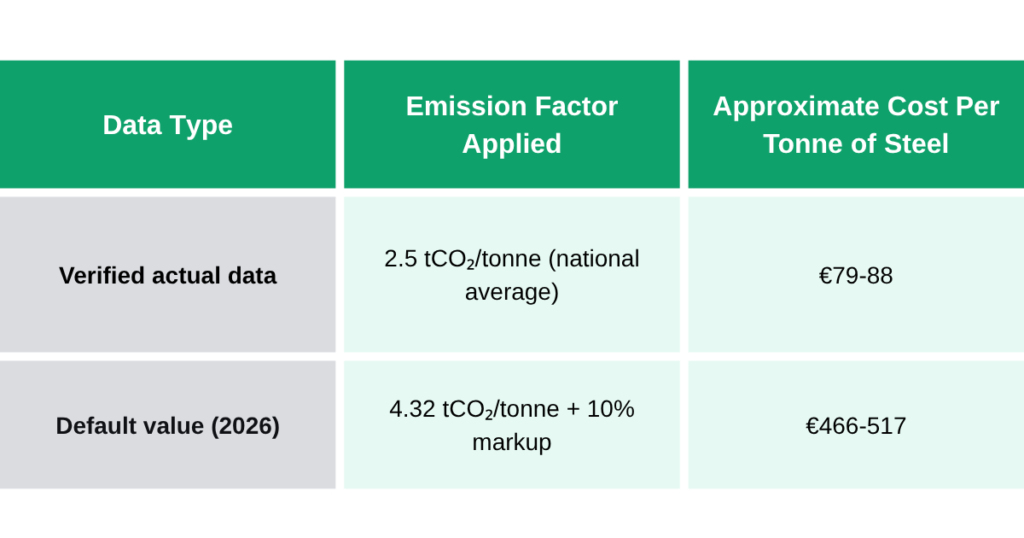

Default Values vs. Verified Data: A Massive Difference

The most critical strategic decision for Indian exporters is whether to invest in emissions verification. The cost difference is staggering:

Without verified data, your product could face carbon costs nearly six times higher than competitors who provide proper documentation.

The Default Value Penalty Schedule

CBAM Certificate Price Rules for Suppliers and the default value penalty schedule are as follows:

- 2026: 10% markup on default values

- 2027: 20% markup on default values

- 2028 onwards: 30% markup on default values

This means waiting to address compliance will only make the problem more expensive.

Actionable Steps: How Indian Exporters Can Prepare and Mitigate Risks

Indian exporters must treat EU CBAM for Indian exporters as a strategic priority. Here is a practical 2026 readiness roadmap:

- Map Exposure and Forecast Impact Calculate your EU export volumes by CN/HS code and estimate embedded emissions using EU methodologies or provisional tools. Model potential certificate costs at current ETS prices (monitor weekly/quarterly averages).

- Build Robust Carbon Accounting Systems Implement plant-level monitoring of direct (Scope 1) and indirect electricity (Scope 2) emissions. Adopt EU-approved calculation methods early. Specialized CBAM Reporting Tools for automated data collection and reporting can streamline supplier and internal processes. Use available CBAM Resources to automate data collection and reporting for streamlined internal processes.

- Prepare for Third-Party Verification Engage accredited verifiers familiar with CBAM/EU ETS rules. Ensure data is traceable, auditable, and retained for at least five years. Utilizing a digital CBAM Declaration Generator can help ensure your data is formatted correctly for official submissions. Start collecting 2026 production data now for the 2027 declaration.

- Engage EU Buyers Proactively Offer verified emission reports voluntarily. Robust CBAM reporting ensures you can negotiate contracts that fairly allocate costs, include data-sharing clauses, and reward lower-carbon production.

- Explore Carbon Price Deductions Although India lacks a full ETS, document any existing or future carbon-related payments (e.g., state-level measures or energy taxes) that could qualify for partial relief.

- Decarbonisation Strategy Invest in energy efficiency, renewable power purchase agreements (PPAs), green hydrogen pilots, or technology upgrades. These reduce future CBAM exposure and enhance competitiveness. Leverage government schemes for green steel or aluminium.

- Leverage Government and Industry Support Monitor Ministry of Commerce, Steel Ministry, and industry bodies (e.g., FICCI, CII) for guidance or potential support measures. Participate in India-EU technical dialogues.

- Risk Mitigation for MSMEs Collaborate with larger players or industry associations for shared verification platforms. Consider grouping for data services to lower costs.

Strategic Opportunities Beyond Compliance

While challenging, the EU carbon levy and the shift in EU CBAM Global Trade can drive positive transformation:

- Green Competitiveness: Early movers in low-carbon production can command premiums and secure preferred-supplier status.

- Diversification: Strengthen presence in non-EU markets while upgrading for Europe.

- Innovation and Finance: Access to green bonds, climate funds, or technology partnerships.

- Policy Alignment: India’s push toward its own carbon market or mechanisms could eventually enable mutual recognition, reducing net CBAM burden.

Companies that treat CBAM as a catalyst for modernisation will emerge stronger, not just compliant.

Final Call to Action for Indian Exporters

The carbon border tax EU is now a commercial reality. With the definitive regime active and the first major declaration deadline in September 2027, Indian exporters—especially in steel and aluminium—cannot afford delay. Start by auditing your emission profile, engaging buyers, and building verifiable data systems today.

The EU market remains valuable, but success in 2026 and beyond will belong to those who combine compliance excellence with genuine decarbonisation. Monitor official EU CBAM updates, consult legal and technical experts, and align internal strategies with national efforts for a coordinated response.

By acting decisively, Indian exporters can turn the EU carbon levy challenge into a driver of sustainable growth and enhanced global competitiveness. The window for preparation is narrow—seize it now to protect and future-proof your EU exports.