CBAM reporting for Indian exporters are changing so fast and it is very important for them to be fully ready for CBAM compliance. In this blog, we decode CBAM readiness for Indian exporters in 2026.

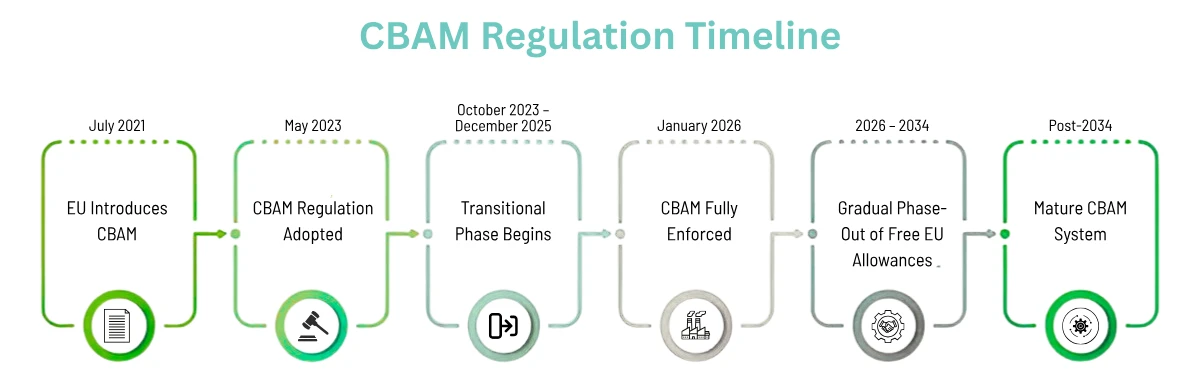

CBAM reporting for Indian exporters has changed from January 1, 2026 as it has become mandatory. Moreover, there are some other major changes in the CBAM regulations for exporters who are exporting CBAM-listed products made of Iron and Steel, Aluminium, Cement, Fertilisers, and Electricity. EU Carbon Border Adjustment Mechanism was introduced to prevent carbon leakage and ensure unbiased market access for all.

What is CBAM?

EU Carbon Border Adjustment Mechanism was introduced to prevent carbon leakage and its mirrors EU ETS. While ETS is applicable to companies affiliated to the EU, CBAM is applicable to all countries and companies that export carbon-intensive products made of Iron and Steel, Aluminium, Cement, Fertilisers, and Electricity.

Anyone who does not mandatorily comply with CBAM from January, 2026 will face penalties, witness shipment blockage, lose access to EU market and won’t remain competitive.

Although the responsibility to submit the CBAM report lies with EU importers, Indian manufacturers will be immensely impacted due to rules of CBAM Reporting for Indian Exporters. Under this carbon pricing mechanism, suppliers have to accurately collect all embedded emissions data and submit the report to the importer who will further submit the report to the EU authorities.

Sectors Under CBAM Reporting for Indian Export

Currently, only the six most carbon-intensive sectors are covered under the CBAM Reporting for Indian Exporters. These sectors pose the greatest risk of carbon leakage.

- Iron and Steel

- Aluminium

- Cement

- Fertilisers

- Hydrogen

- Electricity

CBAM Compliance for Indian Manufacturers

CBAM compliance for Indian manufacturers is an opportunity for them to decarbonise and reduce carbon emissions. Although, CBAM tax will first be imposed on importers, suppliers are not exempted. Here is a look at readiness for CBAM Reporting for Indian Exporters:

Maintain data accuracy: Under the CBAM compliance for Indian manufacturers, it is very important to maintain data accuracy and hygiene. Collecting accurate carbon emissions data and submitting error-free reports can help in tax avoidance and penalty free trade with the EU. Most Indian manufacturers lack systems and infrastructures to collect accurate emissions data. This also means engaging with multiple local vendors to gather accurate data and ensure a transparent supply chain.

Timely CBAM submission: A quarterly report must be submitted as per the CBAM regulations for exporters in India. Suppliers must have a robust data collection system that can ensure timely compliance. This means uninterrupted trade without shipment blockage or penalties on buyers in the EU. However, timely compliance depends on CBAM compliant data collection infrastructure and structured report generation by suppliers.

Maintain data audit trail: Under the CBAM reporting requirements, the EU-accredited agency will audit the data collection trail that involves suppliers and their local vendors. Hence, suppliers must keep all the past data collection and related documents and records ready for auditing purposes and verifications, as mandated under the CBAM regulations for exporters.

Identify hotspot and reduce emissions: The supplier should be able to analyse and identify all emission hotspots to reduce the climate impact. This is the main goal under the CBAM reporting for Indian exporters.

Predict Carbon tax and reduce: Apart from all these readiness, suppliers and importers must have a fair idea of carbon tax that could be imposed on them. This allows suppliers to prepare well and align their business interests in the EU.

Embedded emissions calculation: CBAM is data hungry and it asks for direct, indirect and upstream emissions data. Suppliers must invest in technical expertise that can ensure accurate calculations of direct emissions, indirect emissions, and upstream emissions. Because this will impact the carbon tax to be paid by importers.

Monitoring, Reporting & Verification (MRV): CBAM regulations for exporters mandate that emissions data must be independently verified by EU-recognised or ISO-compliant verifiers before it can be used in official CBAM declarations from 2026.

This means investing in:

- Digital MRV systems

- Carbon accounting software

- Documentation trails that are audit-ready

Without this, exporters risk having EU importers default to higher assumed emissions values — resulting in higher CBAM costs.

CBAM Reporting for Indian Exporters: Check Your CBAM Readiness

CBAM readiness depends on many factors that are highly interconnected. Here is how suppliers can check their CBAM readiness:

CBAM scope check: So far, only 6 sectors including the iron and steel, aluminium, cement, fertilisers, hydrogen and electricity are covered under the CBAM reporting. Furthermore, selected categories and products as per their HSN codes are covered under the CBAM. Hence, it is very important to check if the products you export are covered under CBAM or not.

CBAM required emission data: Under the CBAM regulations for exporters, a lot of direct and indirect emissions data is mandated to be submitted. Under the direct emissions data requirements, suppliers must have actual emissions data of fuel combustion, process emissions, and on-site energy generation. Moreover, under the indirect emissions, suppliers must maintain electricity consumption and grid emission factors (state or national level).

Emissions data quality: Under the CBAM reporting requirements, manufacturers must keep record of at least four years of auditable evidence. The mandatorily required documents are fuel and raw material consumption logs, meter calibration records, electricity invoices, lab test reports (if applicable), emission factors with full citations, and process flow diagrams.

EU-approved calculations: Suppliers must rely only on EU-approved CBAM calculation methodologies and must define their system boundaries strictly as per the regulations.

Verification readiness: CBAM readiness means being ready for EU-accredited third-party verification. As a supplier, you must be ready to host physical site visits in 2026, maintain data traceability and consistency, and have internal teams understand verification questions.

Default value risk assessment: Under the mandatory CBAM reporting rules, the default values have been kept extremely high to act as punitive measures for all the suppliers. It is very important to compare the default values against the actual embedded emissions to determine the carbon tax and pay less.

CBAM regulations for exporters

CBAM Certificate Price Rules for 2026

- From January 2026, the Commission will calculate CBAM certificate price for each quarter as the quarterly average auction clearing prices under the EU ETS. These prices will be calculated during the first calendar week of every quarter.

- In 2026, the quarterly CBAM certificate price will be calculated.

- The relevant auction platforms shall provide all the required information for calculating the CBAM certificate prices for that quarter.

CBAM Certificate Price Rules for 2027

- From January 1, 2027, the CBAM certificate price will be calculated every calendar week on the basis of the weekly average of EU ETS allowance prices.

- Price of CBAM certificates will apply to all CBAM certificates sold to Authorised CBAM Declarants.

- The Commission will publish all CBAM certificate prices on its official website on the first working day.

- Price of CBAM certificates will be made available only to Authorised CBAM Declarants.

Regulation for Verification of Actual Embedded Emissions

Under the CBAM reporting requirements, EU-approved verification has become mandatory from January 1, 2026. Moreover, the suppliers and EU buyers must have emission-related data and verification evidence for the past 4 years since the start of the reporting year for auditing purposes. Here is a look at some major changes in the CBAM verification:

- EU-approved verifiers must conduct physical site visits at the installation where goods were manufactured.

- In 2026, physical visit at all locations is mandatory. However, from 2027, the verifier may either replace the physical visit with virtual visit or waive off the visit.

- The verifier can waive visit from 2027 only after visiting once in 2026 and it does not compromise the data credibility.

- The physical visit should be carried every two years at least.

- The verifiers must analyse all data and cross-check for any misstatements and inaccuracies in the submitted report. Moreover, the verifier has to apply a risk-based approach to reach any opinion.

- The submission and review of the verification reports will be done using a single electronic temple given by the Commission only.

- The verifiers can apply materiality threshold (Scope of error) by 5% only.

Use of default values vs actual emissions in CBAM reporting

Default values are conservative assumptions and estimated emissions numbers that could be applicable to a particular production process. The EU has published default values for companies that can not provide the actual emissions data under the CBAM reporting requirements. These are always much higher than the actual embedded emissions values of a product or a company.

Under the CBAM regulations for exporters, using default values will always mean paying more carbon tax than applicable on actual emissions. This is a deliberate design to prevent carbon leakage and discourage use of default values. Exporters and importers are allowed to use the default values from January 2026 but it could mean significant financial consequences.

Under the latest changes for CBAM reporting for Indian exporters, which is applicable from January 2026, the Commission has published the provisional list of default values for all major countries that export to the EU. These default values have been deliberately kept very high to use them as punitive measures and encourage importers and exporters to use actual emission values. There are different benchmarks given for different sectors and products for all the CBAM listed HSN/CN Code.

How does CleanCarbon.ai help in accurate CBAM reporting?

Since the start of mandatory CBAM reporting for Indian exporters, the industry has been in a panic mode. This is also because a lot of companies are now directly bearing the brunt of CBAM reporting. Many are reporting shipment blockage at the EU borders and customs. A lot more companies are also reporting loss of EU buyers due to loss of confidence in suppliers not submitting accurate CBAM data. However, cleancarbon.ai has been helping suppliers and exporters in building strong emissions measurement, reporting, and verification systems, data workflows, contractual clarity with EU partners, and a long-term decarbonisation roadmap is essential for survival in carbon-aware global markets.

What is CBAM reporting for Indian exporters?

Carbon Border Adjustment Mechanism (CBAM) is EU climate regulation meant for all exports of iron and steel, aluminium, cement. Electricity and fertilisers. CBAM reporting asks for carbon emissions data associated with the product and carbon tax is applied on them accordingly.

Who is required to submit a CBAM report?

EU buyer (also known as importer and Authorised CBAM Declarant) is mandated to submit the CBAM report for all imports in the EU from January 2026.

What is the compliance deadline under CBAM regulations for exporters?

CBAM has become a mandatory compliance from January, 2026 for all EU-importers and exporters of carbon intensive products entering the EU. The CBAM reporting is done on a quarterly basis for the shipment sent to the EU.

What happens if CBAM reporting is late?

There will be penalties and increased CBAM taxes on importers and exporters it the CBAM compliance is not done on time.

Is CBAM reporting quarterly or annual?

Importers have to submit quarterly CBAM reports for the imported products every 3 months.

Can exporters submit CBAM reports?

The exporters submits the CBAM report to the EU importer, who further submits the CBAM report to the EU authorities.

How is CBAM tax calculated under CBAM compliance for Indian manufacturers?

CBAM tax is applicable for all CBAM exports to the EU from January 2026 and it is calculated on the basis of EU ETS quarterly average auction prices. In simpler terms, CBAM tax will be a mirror image of the EU’s internal carbon tax rates.

Are default values allowed under CBAM?

Why do default values increase tax?

Why do actual emissions reduce CBAM cost?

Actual emissions are mostly lower than the default values, which means lower carbon tax. Actual emissions are correct and it allows the supplier in reducing its emissions to achieve carbon-neutrality and reduce its taxes in the long run.

What happens from 2026 onward under CBAM compliance for Indian manufacturers?

CBAM has become mandatory from January 2026 and anyone not submitting the CBAM report on time will not be able to do business, could face penalties, witness increased carbon taxes and also suffer shipment blockage.