CBAM is no longer just an EU policy—it’s reshaping global trade dynamics. As the world’s first carbon border tax, CBAM is forcing nations to rethink their climate and trade strategies. But reactions vary widely: while some regions are embracing similar policies, others are pushing back.

CBAM Goes Global, and here’s how the EU, US, and Asia are responding—and what it means for the future of international trade.

CBAM Goes Global: Challenges and Opportunities

1. The EU: The CBAM Pioneer

Strategy: Lead by example

As CBAM Goes Global, the EU is rolling out CBAM in phases (2023-2026), targeting imports of steel, cement, aluminum, fertilizers, hydrogen, and electricity.

Key Implications:

✅ Protects EU industries from “carbon leakage” (companies relocating to avoid climate rules).

⚠️ Trade tensions rising—exporters in developing nations face new costs.

🔮 Future expansion? Indirect emissions (Scope 2) and more sectors could be added.

Trade Impact:

- EU importers must now track and report emissions—adding compliance costs.

- Non-EU exporters must decarbonize or pay up.

2. The US: A Different Approach – No Carbon Tax, But Green Incentives

Strategy: Subsidize, don’t penalize

Unlike the EU, the US has no federal carbon tax—but as CBAM Goes Global, the Inflation Reduction Act (IRA) offers $369B in green subsidies..

Key Implications:

✅ Boosts clean tech (solar, EVs, hydrogen) without taxing imports.

⚠️ Potential clash with CBAM? US steel exported to the EU could face CBAM costs if made with fossil fuels.

🔮 Will the US adopt a CBAM-like policy? Unlikely soon, but states like California may experiment.

Trade Impact:

– US exporters benefit from IRA subsidies but may still face CBAM costs in the EU.

– EU fears the IRA’s subsidies could lure away green investments.

3. Asia: Mixed Reactions – From Resistance to Adaptation

China: Pushback with a Side of Preparation

- Publicly opposes CBAM as “trade protectionism.”

- But quietly prepares by expanding its own carbon market (ETS).

- Long-term play: May impose its own carbon rules on exports.

India: Fighting for Exemptions

- Strongly opposes CBAM, calling it unfair to developing economies.

- Seeks exemptions for least-developed nations.

- Domestic shift? Investing in green hydrogen and renewables to stay competitive.

Japan & South Korea: Cautious Alignment

- Exploring their own carbon pricing but not yet a CBAM.

- Corporate pressure: Steelmakers (POSCO, Nippon Steel) are investing in low-carbon tech to avoid EU penalties.

Trade Impact:

- Carbon-intensive exporters (India, Vietnam) face the biggest risks.

- Tech leaders (Japan, Korea) may gain an edge with early decarbonization.

The Bigger Picture: A Fragmented or Unified Global System?

Scenario 1: “Carbon Club” Formation

- The EU, UK, Canada, and others align on CBAM-like policies, creating a “climate trade bloc.”

- High-emission exporters face trade barriers unless they decarbonize.

Scenario 2: Trade Wars & Retaliation

- Countries like China and India impose counter-tariffs on EU goods.

- WTO legal battles could stall climate progress.

Scenario 3: A Global Carbon Market Emerges

- UN or G20 brokers a deal on harmonized carbon pricing.

- Clean exporters (Norway, Chile) benefit, while laggards pay more.

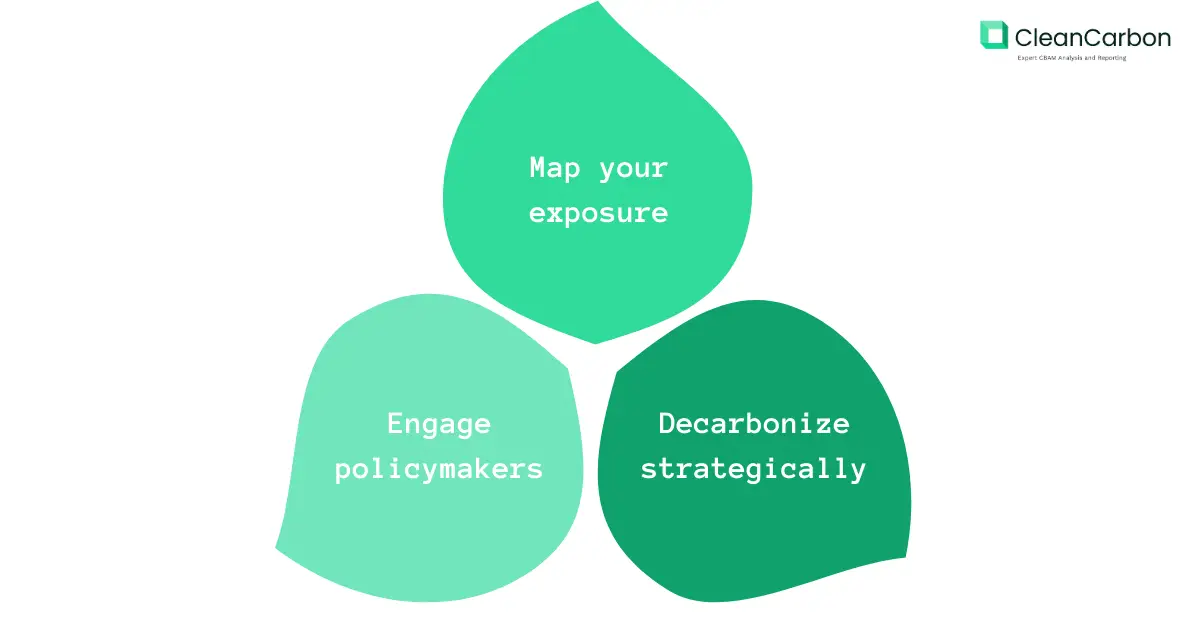

What Businesses Should Do Now?

1️⃣ Map your exposure – Does your supply chain face CBAM costs?

2️⃣ Decarbonize strategically – Switch to renewables, improve efficiency.

3️⃣ Engage policymakers – Advocate for fair but firm climate trade rules.

Final Thought: A New Era of Climate-Driven Trade

CBAM is just the beginning. The question isn’t if carbon costs will reshape global trade—but how fast, and who will lead?

Where does your region stand? Share your insights below.